(来源:智堡Mikko)

Waller演讲

Waller笑称上次(2月)的演讲像是已经过去了一年之久……谈到就业问题时,他说目前的就业及格线是“0”——由于劳动力零增长(移民和退休),现在每月只需新增零个就业岗位就能维持失业率稳定,单月就业负增长不再是绝对的衰退信号。如此环境中,雇主们正在“走钢丝”——因为之前招人太难所以现在不敢裁员,又因为对未来经济没底所以不敢招人。

这次演讲里有不少无奈的自嘲,倒是跟最近diss研究者的风气迎合上了。

"So what happens next? Let me stipulate that I believe economic forecasting is hard even in normal circumstances. I am tempted to say it is a bit like batting averages in baseball, where an excellent result is failing two-thirds of the time, but that wouldn't be fair to baseball—we forecasters have an even lower rate of success."

预测经济就像棒球击球率,失败三分之二都算优秀;但这对棒球不太公平,因为我们经济预测者的成功率其实更低。

对通胀预期的重视和强调也符合此前联储其他官员的调性。

Then there is the issue of how the oil shock, piled onto the lingering effect from import tariffs, affects expectations of future inflation. The standard practice for policymakers is to look through shocks like this that temporarily elevate inflation. But what happens when there is a sequence of these shocks? In 2021 and 2022, the pandemic-induced demand and supply chain constraints were each considered one-off shocks that initially led me to look through their upward pressure on prices. But, ultimately, this series of shocks pushed up inflation to near 9 percent by one measure, longer-range inflation expectations started to move up, and the Federal Reserve took action. Learning from that experience, I will be cautious when faced with a sequence of transitory shocks. While intellectually it makes sense to look through each shock, with a sequence of shocks, policymakers need to be more vigilant. This is because if the shocks hit one after another, they will keep inflation elevated for quite some time. The standard "look through" can become problematic if businesses and households start to believe inflation is persistently high and it affects their price- and wage-setting behavior.

面对单一冲击(如关税),美联储通常选择“忽略其短期影响”(也就是看穿);但如果疫情、关税、原油暴涨接连发生,“连续冲击”会彻底改变大众的通胀预期,再选择无视将面临灾难性后果。

High inflation and a weak labor market would be very complicated for a policymaker. If I face this situation, I'll have to balance the risks to the two sides of the Fed's dual mandate to determine the appropriate path of policy, and that may mean maintaining the policy rate at the current target range if the risks to inflation outweigh those to the labor market.

目前短期看来Waller更重视通胀风险。

褐皮书

4月的褐皮书对比2月的有几个变化:

2月份的不确定性主要集中在关税政策演变和恶劣的冬季天气;时至今日,“中东冲突”成为引发不确定性的首要因素,导致许多企业在招聘、定价和资本投资上采取了“观望”态度。

成本驱动因素从“关税”蔓延至“全面能源冲击”,虽然整体价格增长仍被定性为“温和”,但所有辖区都报告称,由于中东冲突,能源和燃料成本急剧上升。这引发了连锁反应,导致货运、物流以及塑料、化肥等石油基产品的价格大幅上涨,投入成本的增长普遍超过了销售价格的增长,从而压缩了企业的利润空间。

就业依旧保持稳定至略有增长的态势,人员流失率低。边际变化在于用工形式的偏好转变:由于企业对承诺提供永久职位持谨慎态度,多个辖区指出对临时或合同工的需求增加。2月份企业更多强调引入AI是为了“提高生产力”而非替代工人;而在4月份,报告明确指出由AI驱动的生产力提升已经使许多公司能够“推迟或减少招聘”。

Logan谈缩表

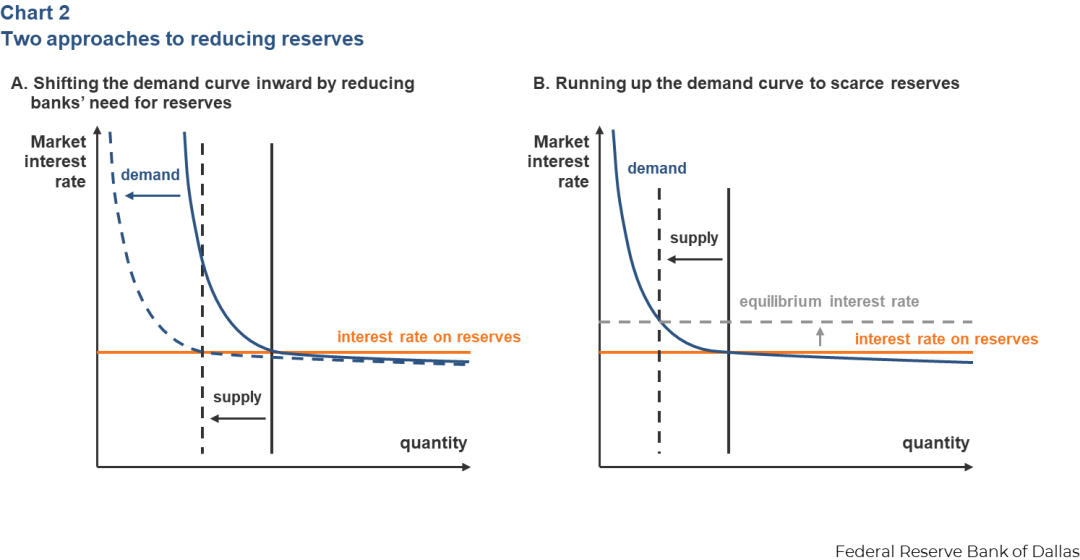

继此前Miran谈资产负债表的未来选项以后,Logan也加入了讨论。演讲中提到了两种方法:

If we reduce banks’ need for reserves so that banks shift the demand curve inward, we’re still meeting banks’ demand. If we run up the demand curve and return to scarce reserves, we’re pushing up market rates relative to IORB and putting a price on reserves that banks don’t face today.

要么是减少银行的准备金需求,要么是回归稀缺准备金。

Logan支持前者,她提到几个点:

元股证券:ygzq.hk一,没成本:

满足银行的准备金需求对美联储来说几乎没有什么成本,因为随着时间的推移,联储从支持准备金的资产上赚取的利息,与支付出去的利息(IORB)是相匹配的。

中通快递-W(02057)发布公告,于2025年11月18日该公司斥资308.06万美元回购16.27万股,回购价格为每股18.74-18.99美元。

二,逼银行在准备金问题上抠抠索索,只会平添金融稳定风险(搞钱荒):

Pressing banks to economize on reserves would only increase risk in the financial system.

三,反对搞准备金计划经济

To avoid those challenges, there have been proposals recently to give every bank a quota on reserves and pay interest only up to the quota. That would stabilize demand, help control rates and reduce the cost to banks, but quotas are a form of central planning. The government would be allocating a valuable resource among private firms instead of letting the free market speak. I don’t think I need to explain to you the drawbacks that could have for innovation, growth and competition.

四,现有监管的问题——低效率

某些流动性监管规定可能会迫使银行持有准备金缓冲,但随后又在危机发生时阻碍银行动用这些缓冲资金。

五,支持通过贴现窗口促进信贷:

If banks are confident they can monetize assets through the Fed when needed, they could choose most of the time to hold fewer reserves and more non-reserve assets such as loans.

如果银行确信在需要时可以通过美联储将资产变现,他们就可以在多数时间选择持有更少的准备金,并将资金转而投向贷款等非准备金资产。

监管变化

1.降低了资本要求,活钱更多。

2.活钱更多,放贷能力就强,资本配置活动也可能加强(回购、并购)。

3.房贷利率有望下降,新规把房贷的风险权重和贷款价值比(LTV)挂钩了。

4.其他的一些风险权重和技术性变化,此处不赘述。

5.总体判断就是未来货币增长不看央行看银行。

⬇️欢迎加入笔者的星球⬇️

左手多资产、右手AI

便宜、轻量化

现有智堡会员/AI用户无需再购买星球,如果非要再购买,您吉祥……星球提供每天公众号的提及内容链接及文件,和智堡会员/智堡AI引擎内的部分内容预览(不超过3%)

重度用户可点击阅读原文认购我们的AI投研系统。

配资网站

]article_adlist-->

海量资讯、精准解读,尽在新浪财经APP

淘配网 | 配资开户 | 实盘账户 | 配资服务提示:本文来自互联网,不代表本网站观点。